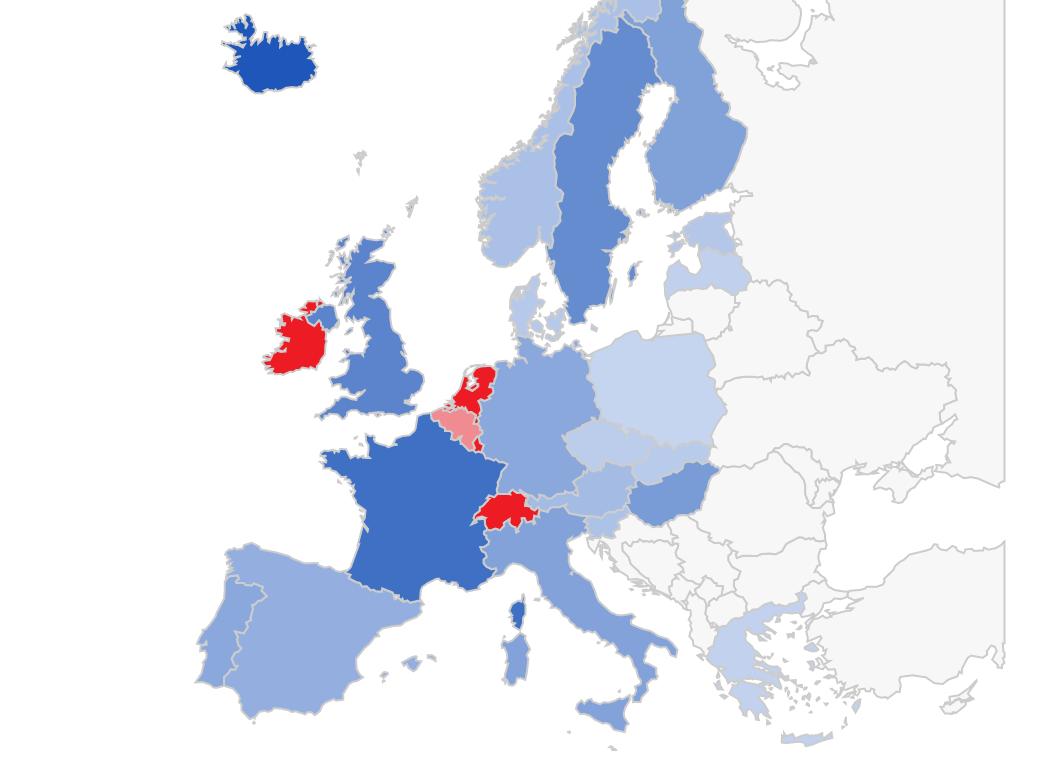

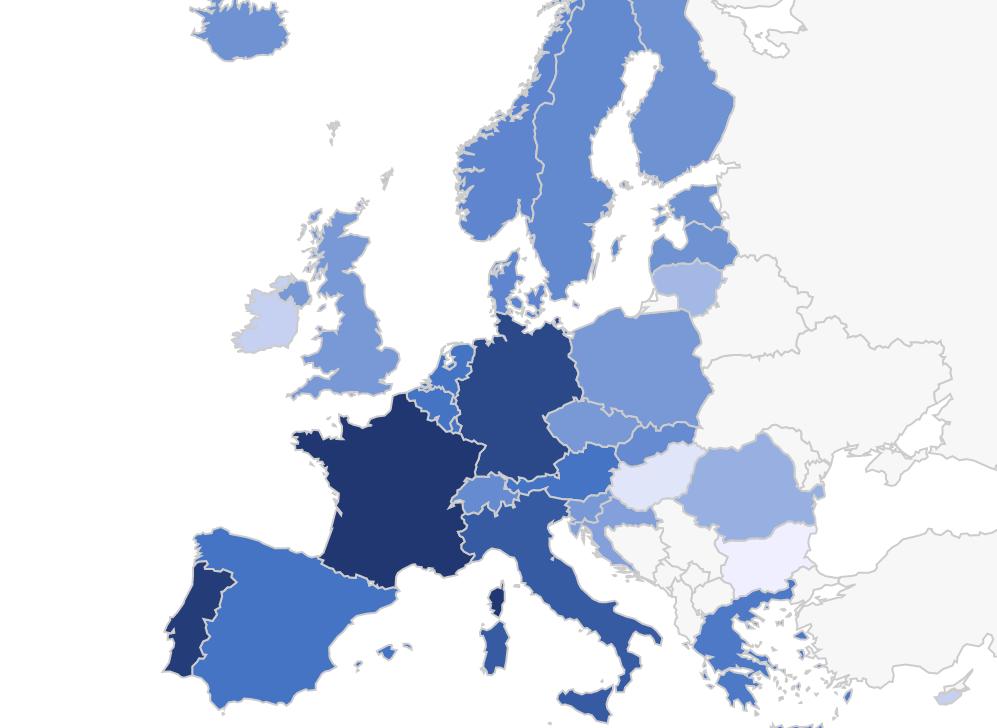

Offshore ownership of real estate

What do we know?

To widen access to knowledge, the EU Tax Observatory maintains a public repository of data and research on tax avoidance and evasion in Europe. We continuously update the content to provide an overview of the current state of empirical research.

Explore recent estimates of the scale of tax avoidance, tax evasion and offshore wealth. Compare estimates across countries, download figures and underlying data or learn more about the methodological approaches used by different researchers.

In the data sources section you find a collection of original data on multinational enterprises‘ tax payments, profits and activity, cross border wealth, and tax rates and rankings which researchers have used in their work.

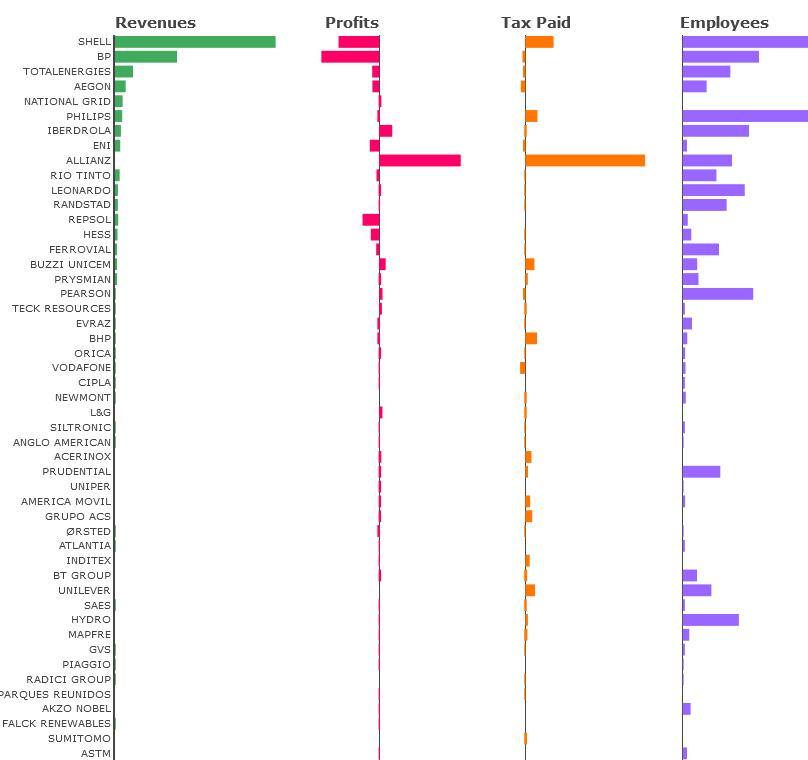

The Public Country-by-Country Reports Explorer

Banks' country-by-country reporting

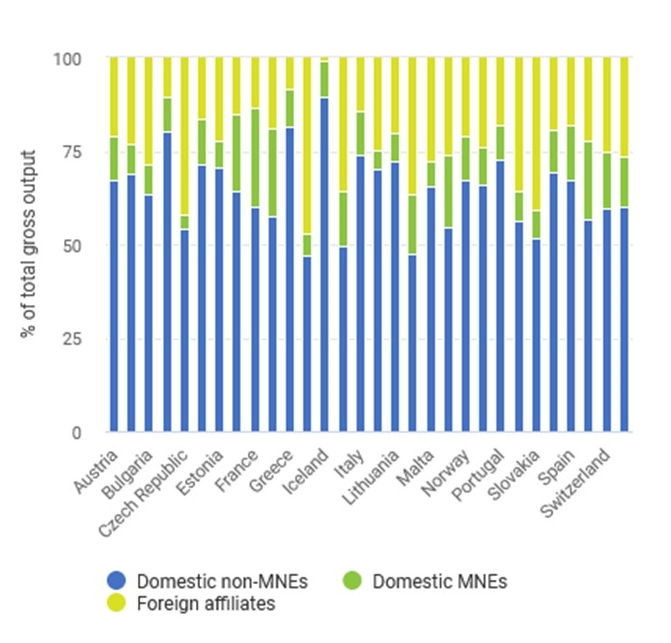

Multinational enterprises' profits and activity

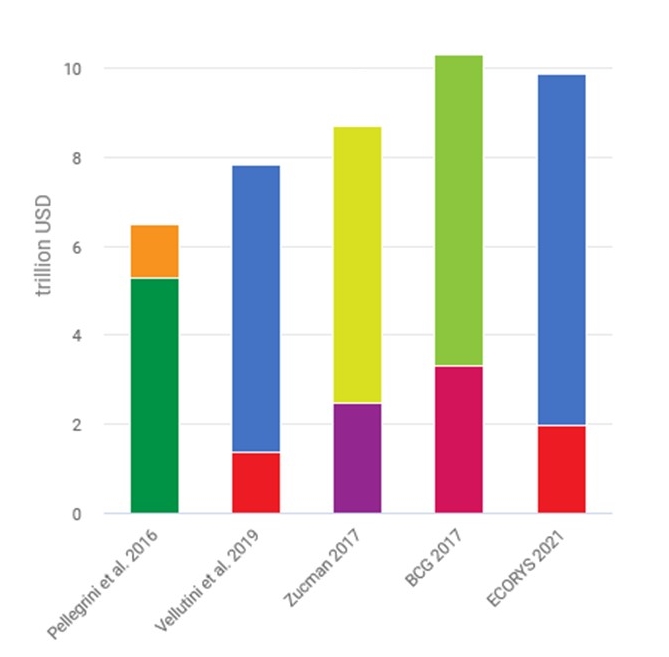

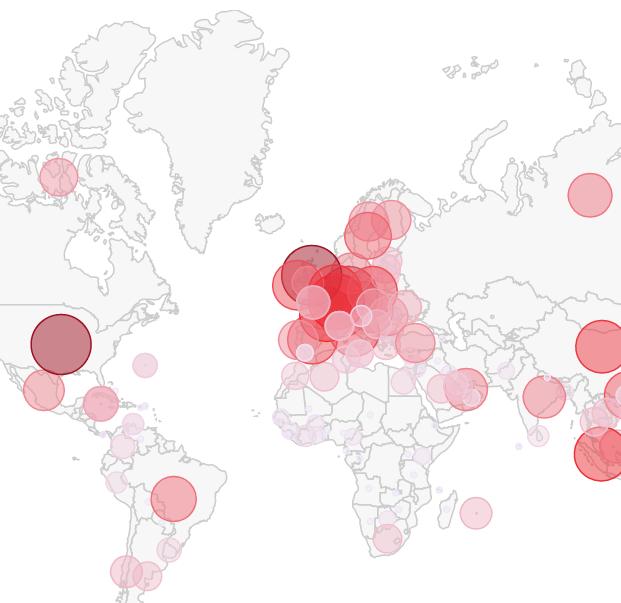

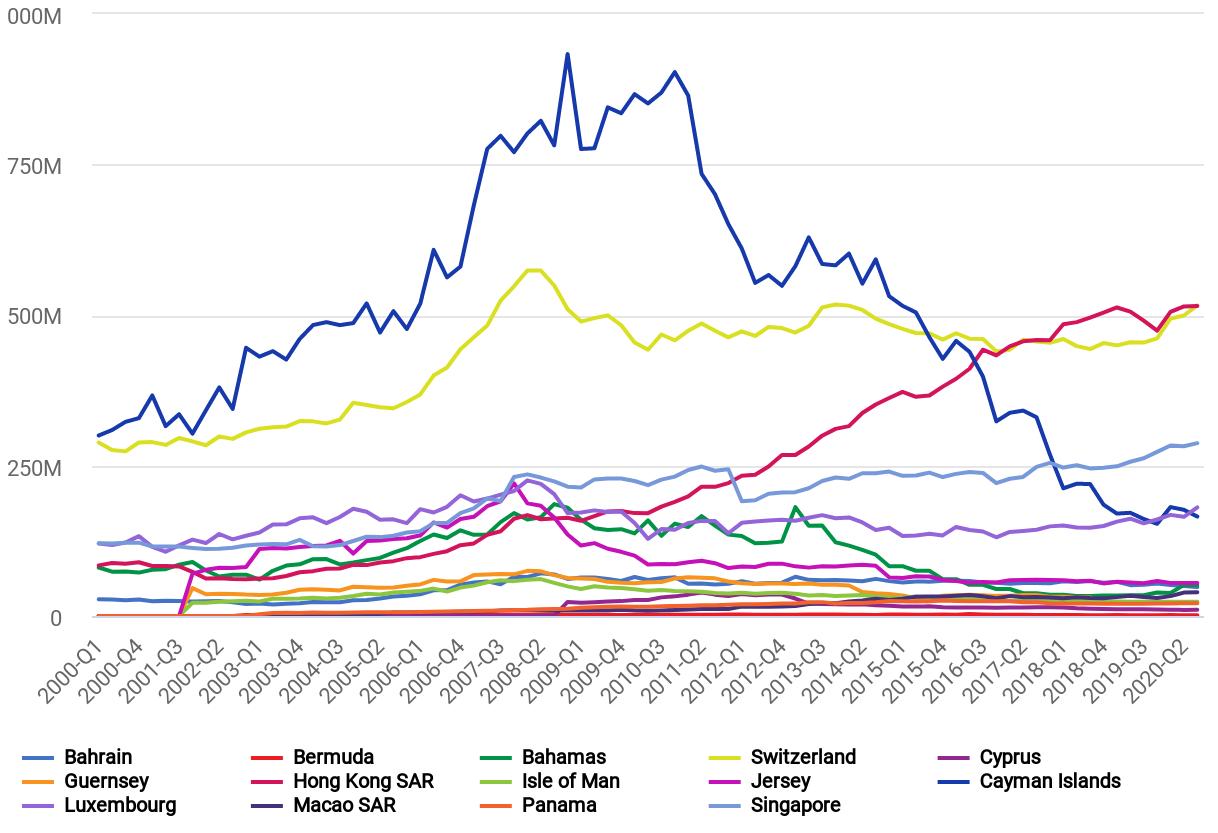

Cross-border wealth

Tax rates and rankings

In this section, you find summaries of recent empirical research on corporate tax avoidance and tax evasion by individuals. Our selection covers reports, working papers and peer-reviewed articles which analyse the scale and channels of tax avoidance and evasion, evaluate the effectiveness of countermeasures or assess new policy proposals.

1.1. The scale of tax avoidance

1.2. Channels of tax avoidance

1.3. Countermeasures to corporate tax avoidance

1.4. Effects of corporate tax avoidance

2.1. The scale of tax evasion by individuals

2.2. Channels of tax evasion

2.3. Countermeasures

Newsletter

Subscribe