Who owns offshore real estate? Evidence from Dubai cross-border real estate investments

Research by Alstadsæter, Planterose, Zucman & Økland 2022

Summary

The paper studies the effect of shifting profits to tax havens on the compensation of employees paid by publicly listed US multinational companies to their employees. Theoretically, higher after-tax profits might partly be shared with employees which would suggest a positive impact of profit shifting on employee pay. However, hiding profits in offshore financial centers might also decrease the bargaining power of workers and thus wages as they are no longer aware of the real size of profits. In other words, firms gain an informational rent. Souillard tests which effect dominates empirically.

An innovative contribution of the author is to distinguish between different kinds of employees: on the one hand, those with executive positions (CEOs and CFOs) should enjoy a larger positive effect – especially those paid on an after-tax basis – as their compensation is allowed to fluctuate to reflect the results of the firm. The negative effect on them should be negligible, as they are able to observe the real financial results of the firm, and so do not lose bargaining power. For non-executive employees, in contrast, the situation is reversed: their wages are often fixed and less likely to respond to an increase in profits. Moreover, as they have no access to the true financial performance of the firm, an informational imbalance is introduced, which decreases their bargaining power.

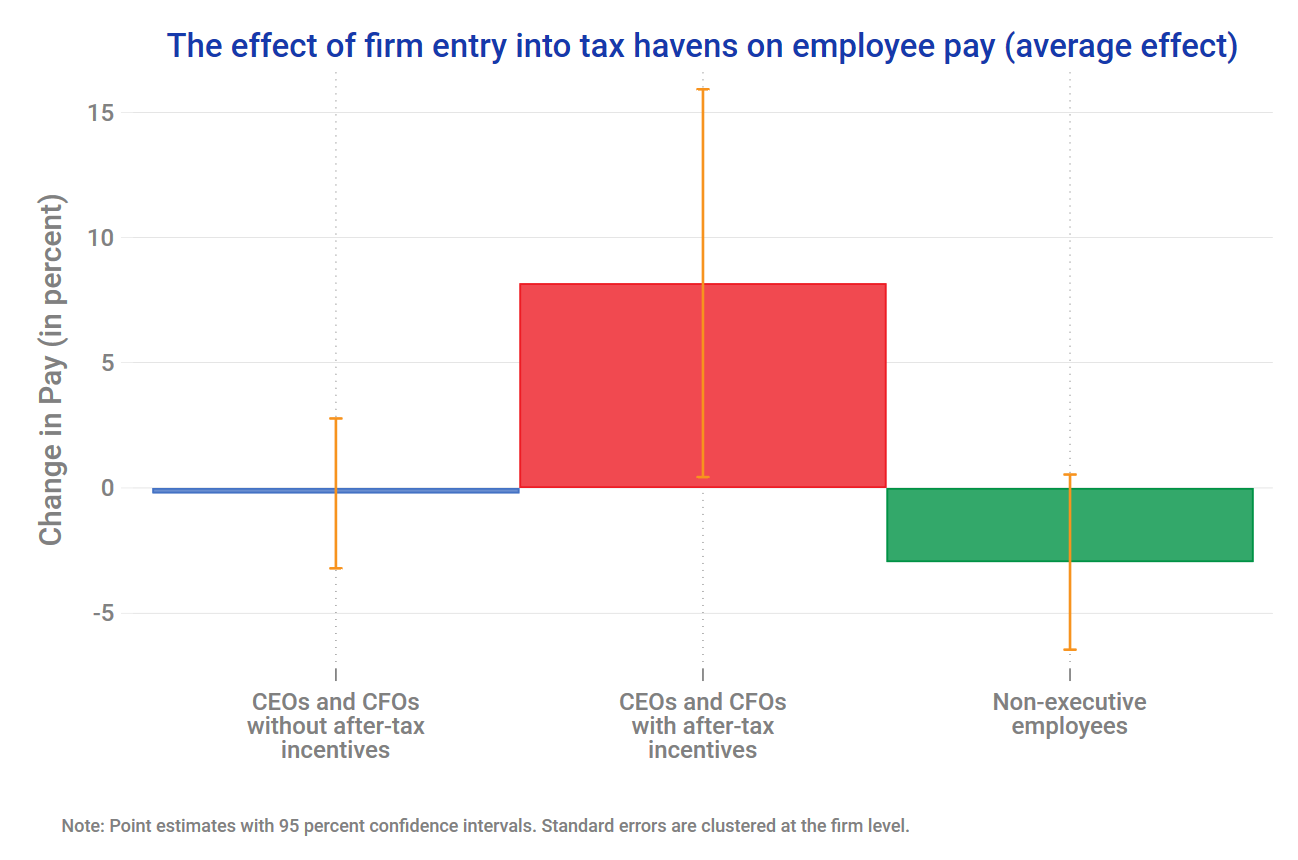

Souillard tests these hypotheses based on a sample of U.S. firms listed on the S&P 1500 index between 1993 and 2013. He analyses the evolution of wages before and after firms start operations in offshore financial centers which he interprets as an intensification of profit shifting. Results suggest differential effects on CEOs and CFO and non-executive employees. Firms’ entry into offshore financial centers increases the compensation of CEOs and CFOs with after-tax incentives by 8%, while there is no change in the compensation of those executives whose pay structure is determined before taxes. Payments to non-executive employees decrease by 3%. The author further finds that the observed effects on employee compensation are more pronounced for firms holding more intangible assets suggesting that intangible assets fuel and facilitate profit shifting.

Key Results

Policy implications

Data

The paper constructs a novel database by merging ExecuComp data on compensation of executives with the Compustat database of firms’ financial statements and Exhibit 21 (a form each US-listed company has to file every year) data on the geographical distribution of firms’ subsidiaries. The final database thus contains observations at the level of executives in individual firms and years, including the compensation scheme, the financial results of the firm, and the network of subsidiaries.

Methodology

The theoretical section refers to a Nash bargaining model of wage negotiations, which is a standard way of modeling bargaining power. In this model, the surplus is shared between the firm and the employees, and the respective shares are proportional to each party’s bargaining power.

The empirical analysis is based on an event study design, with a dummy variable that takes the value of 1 if a firm is operating in offshore financial centers in a given year and 0 otherwise. The dummy is interacted with the compensation of different types of employees. The author performs several robustness checks. For instance, by focusing on small tax havens (e.g. Jersey) and ignoring larger ones (e.g. Switzerland), he makes sure that the firms that operate there do so for tax reasons and not for significant economic activity. He further shows that entry into offshore financial centers is associated with a drop of the effective tax rate paid by the firm.

Go to the original article

The working paper is available on Baptiste Souillard’s website.

Who owns offshore real estate? Evidence from Dubai cross-border real estate investments

Hidden in plain sight: Offshore ownership of Norwegian real estate

The role of anonymous property owners in the German real estate market: First results of a systematic data analysis

Homes incorporated: Offshore ownership of real estate in the U.K.