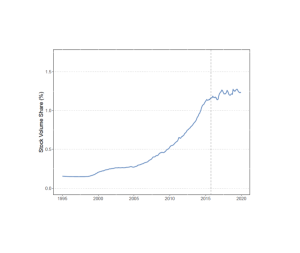

Johannesen, Miethe & Weishaar (2022): Homes incorporated: Offshore ownership of real estate in the UK.

The authors analyze several micro-data sources, from administrative data to offshore data leaks, to reveal the ultimate beneficial owners of real estate in the UK. They find that:

- The market share of offshore corporations increased rapidly between 2005 and 2015.

- Corporations in offshore tax havens were most commonly registered in the British Virgin Islands, Jersey and Guernsey.

> read more about this research

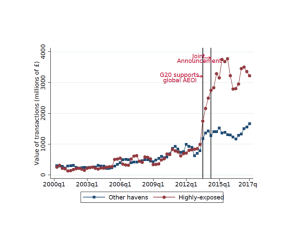

Bomare & Le Guern Herry (2022): Will we ever be able to track offshore wealth? Evidence from the offshore real estate market in the UK.

The authors analyze administrative data on real estate purchases made by foreign companies in the UK and leaked data to trace ultimate ownership for a subsample of transactions. They find that:

- The introduction of the Common Reporting Standard is associated with a significant increase of UK real estate investments from companies incorporated in highly exposed tax havens.

- Global scale estimates suggest that 24% to 27% of the offshore financial wealth fleeing tax havens might have been shifted to real estate.

> read more about this research

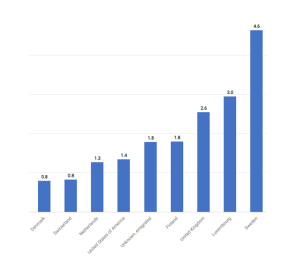

Badarinza & Ramadorai (2018): Home away from home? Foreign demand and London house prices.

The authors analyze several data sets of housing transactions and country-level economic and political risk measures to explore the influence of foreign risk on London house prices. They find that:

- Foreign capital accounts for 7.9% of the total variation in London house prices.

- At least 85% of residential property purchases by foreign companies in London occur through an offshore corporation such as Jersey (26.6%), Isle of Man (14.5%) and Guernsey (13.4%)

> read more about this research

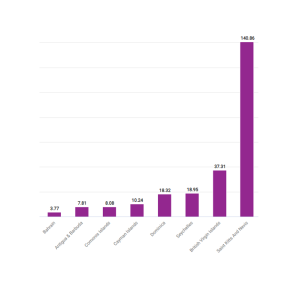

Sá (2016): The effect of foreign investors on local housing markets: Evidence from the UK.

The author analyses administrative data to explore the effect of foreign investment by overseas companies on the housing market in England and Wales. She finds that:

- An increase of one percentage point in the volume share of residential transactions registered to overseas companies is associated with an increase of about 2.1% in house prices.

- Among the residential property transactions involving a foreign company, most of them were incorporated in tax havens such as British Virgin Islands (33.5%), Guernsey (19.4%), and Jersey (11.5%).

> read more about this research