The state of tax justice 2021

Report by the Global Alliance for Tax Justice, Public Services International, and the Tax Justice Network

Summary

The report presents global estimates of the tax revenue losses due to corporate tax avoidance and personal income tax evasion. Estimates are broken down to a large number of countries including many low-income countries and set in relation to each country’s GDP.

The authors estimate the amount of shifted profits by calculating the difference between reported profits in each country and the counterfactual distribution of profits that would prevail if profits were aligned with economic activity. To do so, they use aggregate country-by-country data published by OECD in 2021 and proxy economic activity by the location and estimated compensation of employees. To account for the incompleteness of the dataset, they extrapolate data for non-reporting countries based on additional data sources. In contrast to the 2020 report, the tax revenue losses are estimated by applying the statutory rate instead of the existing effective rate, which increases the estimated revenue losses. The authors argue that shifted profits would normally be taxed at the statutory rate because the tax-optimizing multinational enterprises (MNEs) would have taken advantage of all tax base narrowing reliefs already.

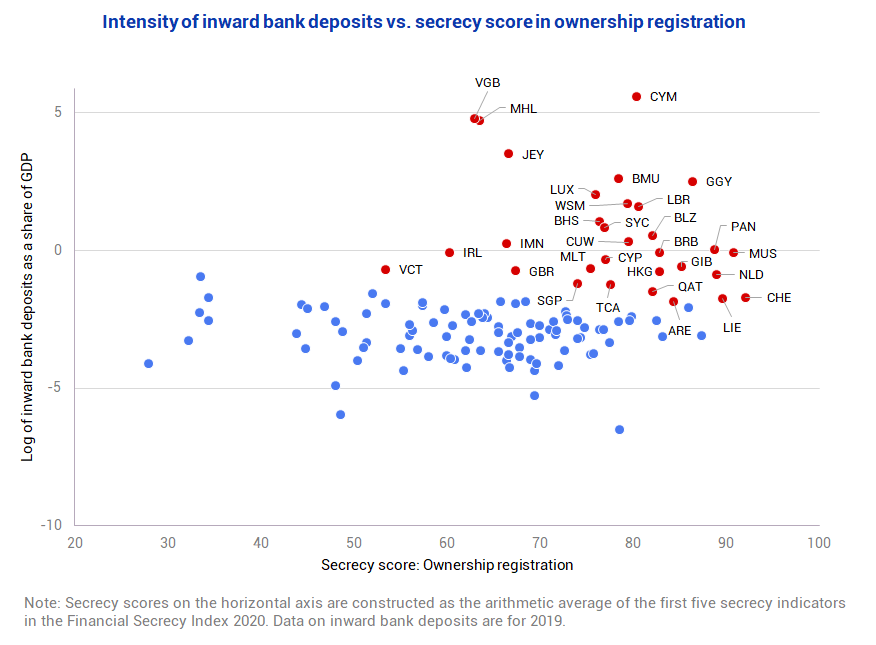

As for tax evasion by individuals, the TJN uses a four-step approach, building on the existing literature using discrepancies in macroeconomic statistics (read more about the discrepancy approach in our summary of Pellegrini et al.). The authors first identify what they call “abnormal deposits” in countries offering some financial secrecy, which is the share of foreign deposits in such countries that is incommensurate to the size of their GDP. The countries of origin of these abnormal deposits are then estimated based on the BIS locational banking statistics. The authors assume that ownership of portfolio assets held offshore is distributed in the same way as the ownership of deposits. Thirdly, they apply the estimated origin country shares to existing estimates of total global offshore financial wealth, to derive the absolute amount of offshore wealth originating from each country. Finally, they derive the tax revenue losses by applying the top bracket personal income tax rates to the offshore assets.

Key results

- TJN estimates that the world is losing over $483 billion a year due to international tax abuse of which $312 billion are due to corporate tax avoidance and $171 billion are due to tax evasion by individuals.

- Higher income countries are responsible for facilitating 99.4% of corporate tax losses.

- Higher income countries lose more tax revenues in absolute terms. However, lower income countries lose a higher share of their collected tax revenue.

- The tax lost in a single year to cross-border tax abuse equals the cost of fully vaccinating the world’s entire population more than three times over.