Offshore tax evasion and wealth inequality: Evidence from a tax amnesty in the Netherlands

Research paper by Leenders et al. 2020

Summary

Guyton et al. estimate the share of income underreporting along the income distribution. They observe that the random audit program of the US Internal Revenue Service (IRS), known as the National Research Program (NRP), allows detecting the simplest forms of tax evasion but fails to capture more sophisticated evasion strategies. As a result, estimations of the scale of tax evasion based on random audit data might suffer from a downward bias as sophisticated evasion strategies might be more frequent among high-income earners who also account for an important share of total income.

For their study, the authors combine three sources of microeconomic data: random audit data, results of targeted enforcement activities and operational audit data. Their first contribution is to shed light on the limitations of random audit statistics when trying to estimate the tax gap, i.e. the difference between taxes theoretically owed and taxes paid. These display a sharp drop in detected evasion at the top of the income distribution. The authors demonstrate that undetected offshore evasion explains this drop in detection by matching random audit data to a sample of U.S. taxpayers who voluntarily disclosed hidden offshore assets in the context of specific enforcement initiatives. Additionly, their research shows that due to resource constraints, IRS investigators often cannot assess the degree of compliance of pass-through businesses.

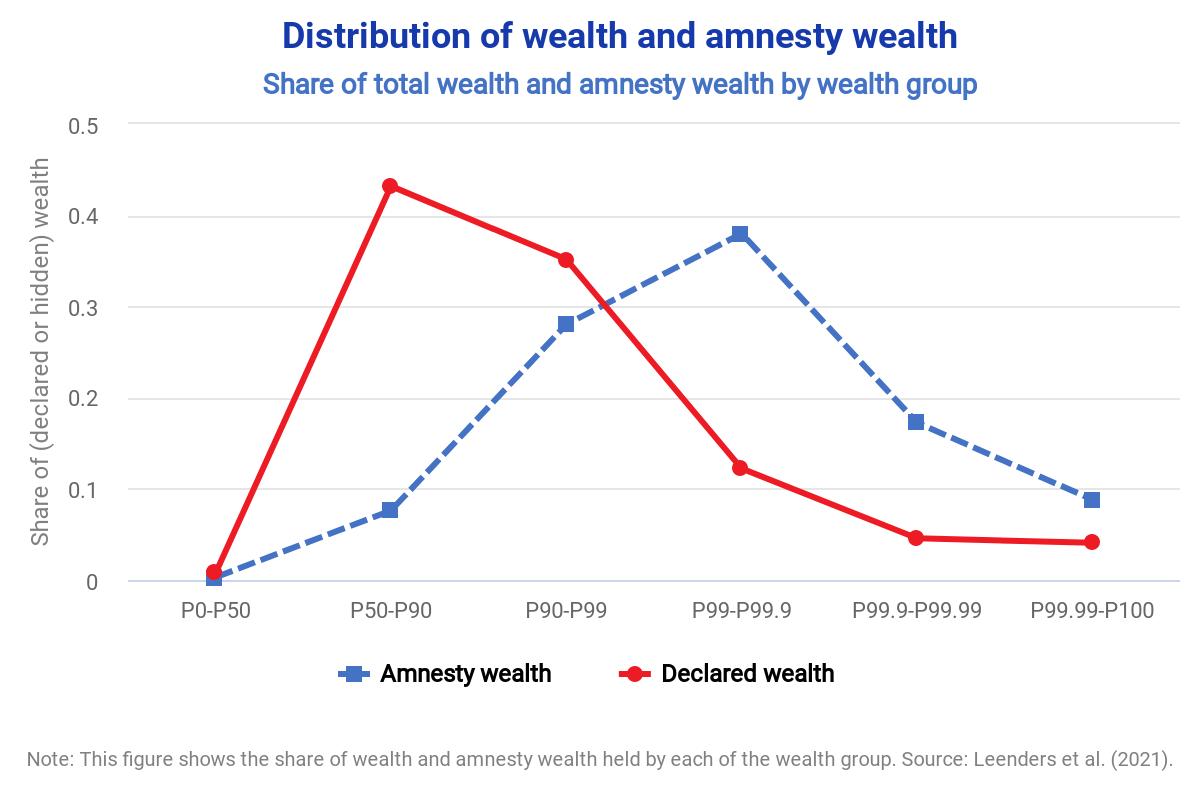

Based on these observations, the Guyton et al. propose a re-estimation of income underreporting for different income groups. While their adjustments have limited impact on the aggregate result of the standard IRS methodology, they are very concentrated at the top: for instance, underreported income is multiplied by 1.8 for the top 0.1% of the income distribution. Their results suggest that the share of underreported income (as a ratio to true income) varies from 7% for the bottom 50% of the distribution to 21% among the top 1%.

Eventually, Guyton et al. adapt a theoretical model from the classical deterrence framework of Allingham and Sandmo (1972) to take into account sophisticated evasion strategies of high-income taxpayers. They demonstrate that in contrast to the standard predictions of the model, random audits cannot uniformly capture non-compliance across the income distribution.

Key results

Policy implications

Data

The authors combine different data sources in their study: random audit data from the National Research Program (NRP) of the IRS and results of operational audits conducted by the IRS as part of the Global High Wealth program. In addition, they use voluntary offshore account disclosure registries, and the Offshore Voluntary Disclosure (OVD) and the Foreign Bank Account Report (FBAR) programs.

Methodology

Guyton et al. provide descriptive evidence of tax evasion based on administrative data and undertake various extrapolations and sensitivity analyses to estimate the share of under-reporting along the income distribution. They reproduce the Detection Controlled Estimation (DCE) used by the IRS to estimate the tax gap from random audit data and develop a theoretical model of the choice to conceal tax evasion from auditors.

Go to the original article

The original article was published by the National Bureau of Economic Research. It can be downloaded from the organization’s website. [pdf]

Offshore tax evasion and wealth inequality: Evidence from a tax amnesty in the Netherlands

The scale of tax evasion by individuals

Tax Evasion at the Top of the Income Distribution: Theory and Evidence

Monitoring the amount of wealth hidden by individuals in international financial centres