Will we ever be able to track offshore wealth? Evidence from the offshore real estate market in the UK

Research by Bomare & Le Guern Herry 2022

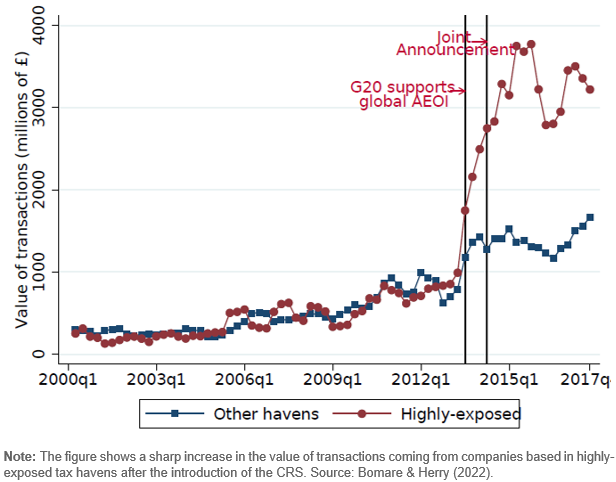

The implementation of the Common Reporting Standard (CRS) was a major step to reduce tax evasion, requiring participating jurisdictions to collect and exchange financial account information on foreign tax residents. At present, the CRS has the drawback of covering only financial assets. This provides an incentive to switch to non-financial assets to avoid reporting. In their study, Bomare & Le Guern Herry examine whether real estate investment in the UK through offshore companies increased as a result of the introduction of the CRS.

They use administrative data on UK real estate purchases by foreign companies. To obtain information on the country of origin of beneficial owners behind the tax haven companies, they use leaked data such as the Panama Papers, the Pandora Papers or the OpenLux. This allows the authors to isolate tax havens “highly exposed” to the implementation of the CRS, i.e. with more than 75% of their company beneficial owners coming from early-adopting countries.

Bomare & Le Guern Herry estimate that £16 to £19 billion have been invested in the UK real estate market between 2013 and 2016 in reaction to the CRS. An extrapolation to the global scale would suggest that 24% to 27% of the offshore financial wealth that left tax havens following the CRS policy were ultimately shifted to real estate.

Key results

Key results

Total value of transactions from companies incorporated in “highly-exposed” tax havens vs other havens

Key results

- In reaction to the implementation of the Common Reporting Standard (CRS), £16 to £19 billion have been invested in the UK real estate market.

- The CRS transparency shock led to a significant increase of UK real estate investments from companies incorporated in highly exposed tax havens.

- Applying the UK estimates to the global scale would suggest that 24% to 27% of the offshore financial wealth fleeing tax havens might have been shifted to real estate.