Homes incorporated: Offshore ownership of real estate in the U.K.

Research by Johannesen, Miethe & Weishaar 2022

The authors analyze real estate ownership in the United Kingdom through corporations in offshore tax havens, as opposed to ownership by foreigners per se. Usually, the beneficial owners of offshore corporations do not show up in land registry data. However, by matching several micro-data sources, from administrative data to offshore data leaks, the authors are able to reveal the ultimate beneficial owners of real estate in the UK.

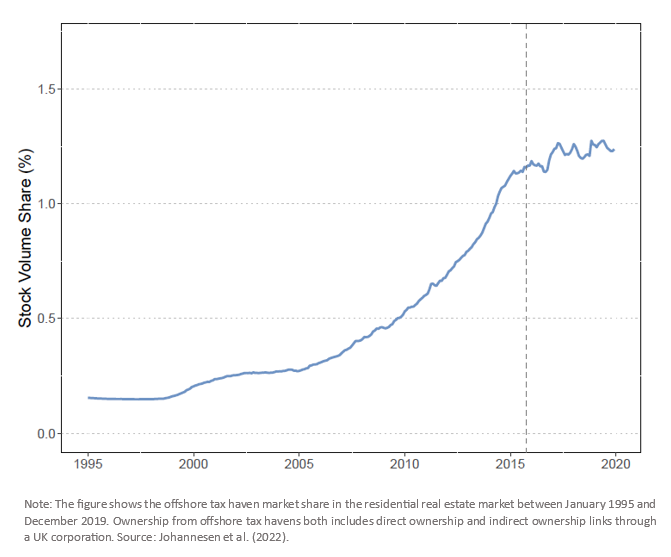

They find that the market share of offshore corporations in England & Wales increased rapidly between 2005 and 2015 and that almost all foreign corporate real estate investment comes from tax havens. In fact, in 2019, corporations in offshore tax havens owned residential properties worth around £50 billion. This is around five times more than the combined holdings of corporations registered in foreign non-haven countries, such as the United States, Japan and France. The offshore corporations were most commonly registered in the British Virgin Islands, Jersey and Guernsey.

Beneficial owners in Asia, Africa and the Middle East account for around 50% of the properties in the UK with nominal offshore owners, much higher than what other sources suggest for offshore financial assets. However, the authors find that 15% of the property investments were residents of the UK, thereby making the UK its own largest “foreign” investor. This suggests an important role for domestic investors buying UK real estate through offshore corporate vehicles.

Geographically, offshore ownership of real estate is concentrated in affluent parts of large cities like Manchester, Leeds and most notably London. There is barely any offshore ownership in rural areas and smaller towns.

Lastly, the authors test the impact of several policies. Their results document that two policies, one about capital gains tax incentives and the other about ownership transparency, caused sharp behavioral responses, with offshore ownership migrating to jurisdictions with low taxation and low transparency. This suggests that both taxation and secrecy are important motives for beneficial owners. Furthermore, the authors demonstrate that the Brexit referendum was followed by an increase in property sales by offshore owners and that offshore ownership has significant real effects on housing markets.

Offshore tax haven market share over time

Key results

Offshore tax haven market share over time

Key results

- The market share of offshore corporations increased rapidly between 2005 and 2015.

- Almost all foreign corporate real estate investment in England & Wales comes from tax havens.

- Corporations in offshore tax havens were most commonly registered in the British Virgin Islands, Jersey and Guernsey.