Base Erosion, Profit Shifting and Developing Countries

Research by Crivelli, De Mooij and Keen 2015

Summary

Crivelli et al. assess to what extent developing countries are affected by corporate tax base erosion, profit shifting, and tax competition. In different regression analyses they test whether the corporate tax base of a country reacts to changes in the domestic and foreign corporate income tax (CIT) rates. They find that an increase in a country’s CIT rates has a negative effect on the country’s tax base. Similarly, they find that decreases in foreign CIT rates also have a negative effect on a country’s tax base. They refer to this effect as “base spillovers” as the country’s tax base reacts to changes in foreign tax policy.

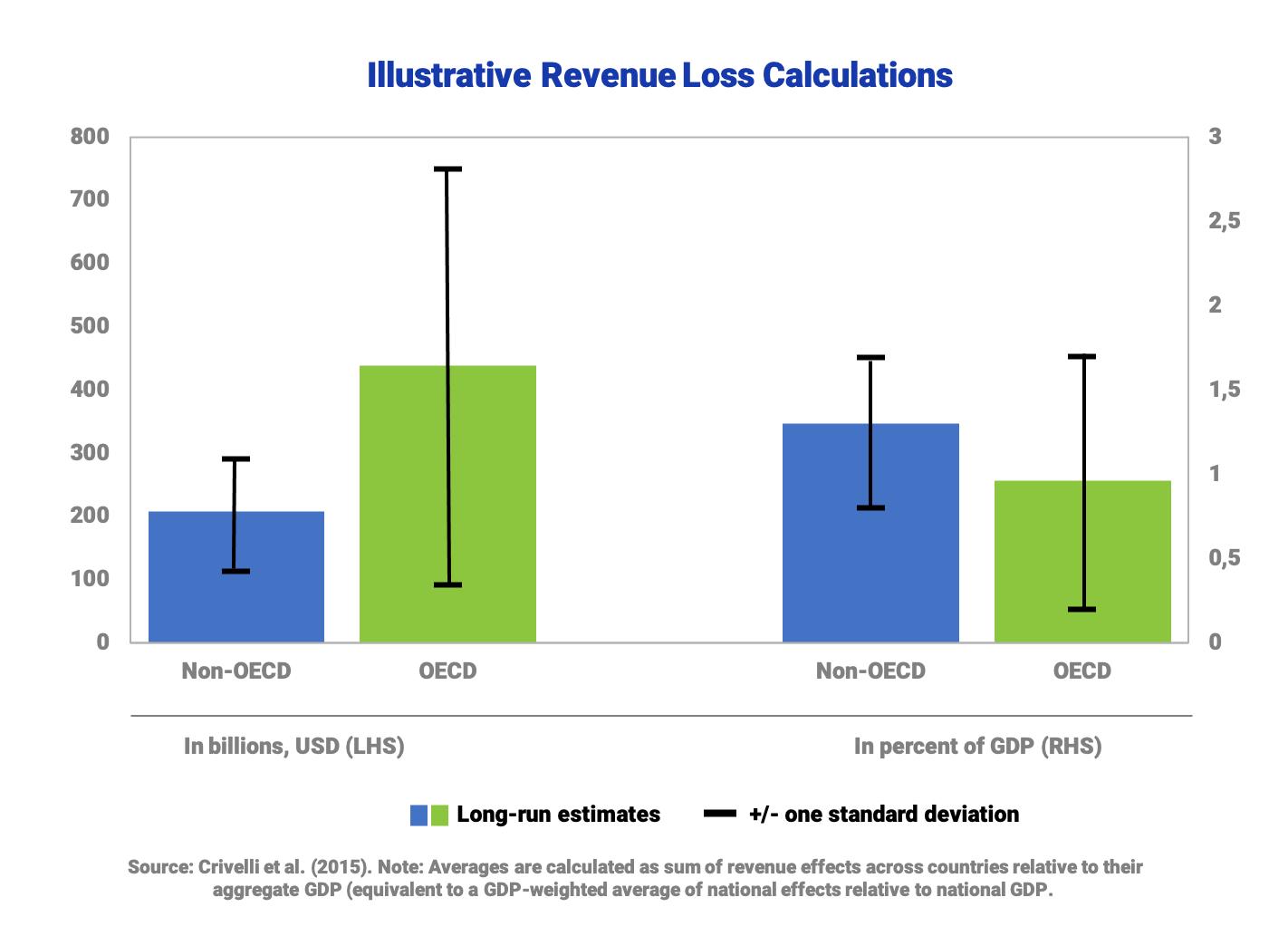

Arguing that base spillovers may be caused by real capital flows but also by profit shifting, they show that changes in the CIT rates of tax havens have a strong negative effect on corporate tax base which they attribute to profit shifting activities. The authors find that non-OECD countries are affected by base spillovers to a similar extent as OECD countries or even more. However, spillover channels differ between the two: while real capital flows seem to dominate for OECD countries, profit shifting seems to dominate the spillover effects for the non-OECD countries. In terms of estimated tax revenue losses, OECD countries lose larger absolute amounts but developing countries seem more severely harmed relatively to GDP. In addition, Crivelli et al. find that countries respond to tax rate reductions abroad by cutting their own tax rate which the authors term as “strategical spillovers”. They show that this effect is particularly strong among OECD members.

Key results

- The results suggest that corporate tax base erosion, profit-shifting and tax competition are as much of a concern for developing countries as it is for OECD countries.

- Profit-shifting seems to dominate the base spillovers for developing countries rather than real investment decisions.

- Relatively to GDP, tax revenue losses are larger for non-OECD countries than for OECD members amounting to 1% and 1.3% of GDP respectively. However, the authors highlight the tentative nature of their estimates.

- Countries respond to tax rate reductions elsewhere by cutting their own tax rates. This response is particularly strong among OECD countries as a one percentage point cut in the average CIT rate abroad is associated with a one percentage point cut in the domestic rate.