Who owns offshore real estate? Evidence from Dubai cross-border real estate investments

Research by Alstadsæter, Planterose, Zucman & Økland 2022

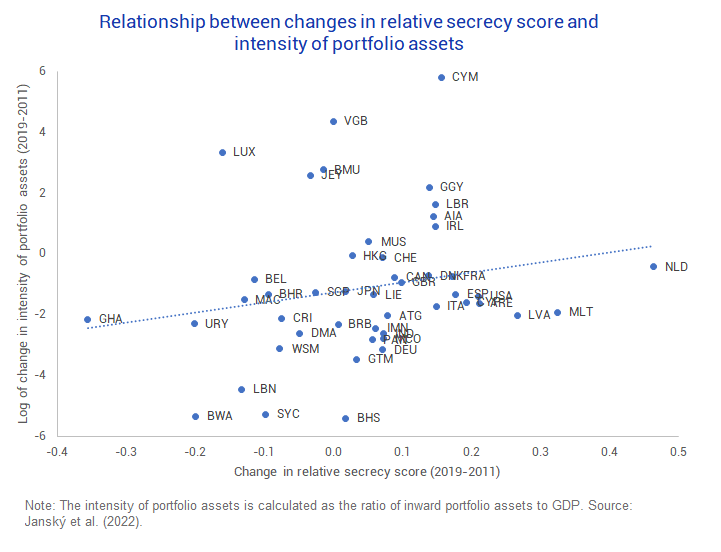

Janský et al. assess how the various financial transparency measures implemented in the past decade impacted the location of cross-border financial assets across countries. Rather than analysing the effect of individual policies, they test whether changes in secrecy scores of the Financial Secrecy Index can explain the location of cross-border portfolio investment and bank deposits between 2011-2020. These secrecy scores combine 20 indicators that measure the opportunities for hiding an investor’s identity, e.g. due to loopholes in a jurisdiction’s ownership registration or a lack of international cooperation.

The authors suggest that an investor’s locational decision between two secrecy jurisdictions depends on the cost of establishing an offshore investment and the probability of being caught and sanctioned and make three theoretical predictions: First, only high-secrecy jurisdictions are used for tax evasion. Second, the impact of changes in secrecy on cross-border financial assets is highly non-linear (i.e. the impact of a unit change in secrecy is greater the larger the change in secrecy). Third, asset holders will only relocate their investment in response to a large-enough change in relative secrecy between two jurisdictions.

For their empirical analysis, the authors harmonise secrecy scores over the available years to obtain a panel dataset for 71 countries. They assess whether a relative change in secrecy between two jurisdictions modified the investment location decisions made by asset holders from third countries. In accordance with their theoretical predictions, they find that investors react to changes in financial secrecy by relocating their assets to high-secrecy jurisdictions becoming relatively more financially secretive. The results suggest that this effect increases with the size of the change in relative secrecy and is stronger for portfolio investment than for bank deposits. Furthermore, the relocation effect seems to be stronger for cross-border financial assets originating from lower-income countries which might indicate a larger illicit component.

Key results

Data

Methodology

Go to the original paper

The working paper can be downloaded from the website of the Social Science Research Network. [PDF]

Who owns offshore real estate? Evidence from Dubai cross-border real estate investments

Hidden in plain sight: Offshore ownership of Norwegian real estate

The role of anonymous property owners in the German real estate market: First results of a systematic data analysis

Homes incorporated: Offshore ownership of real estate in the U.K.