The implementation of the global minimum tax in the EU

In the ongoing debates about the global minimum tax, its compatibility with EU law is frequently put into question. A…

García-Bernardo and Janský estimate the global scale and distribution of profit shifting using country-by-country reporting (CbCR) data. Reviewing the existing models, they advocate for a new approach to better account for the non-linearity of the relationship between the location of MNE’s profits and corporate income tax rates. Their goal is to reflect the fact that MNEs shift disproportionately more profits to tax havens with zero corporate income tax or effective rates below 1% than to other low-tax jurisdictions.

Based on their new non-linear model, the authors estimate that in 2016, MNEs shifted circa 950 billion USD of profits towards tax havens and derive an associated corporate income tax revenue loss of 200 to 300 billion USD. The results further suggest that MNEs headquartered in the United States and China shift profits most aggressively.

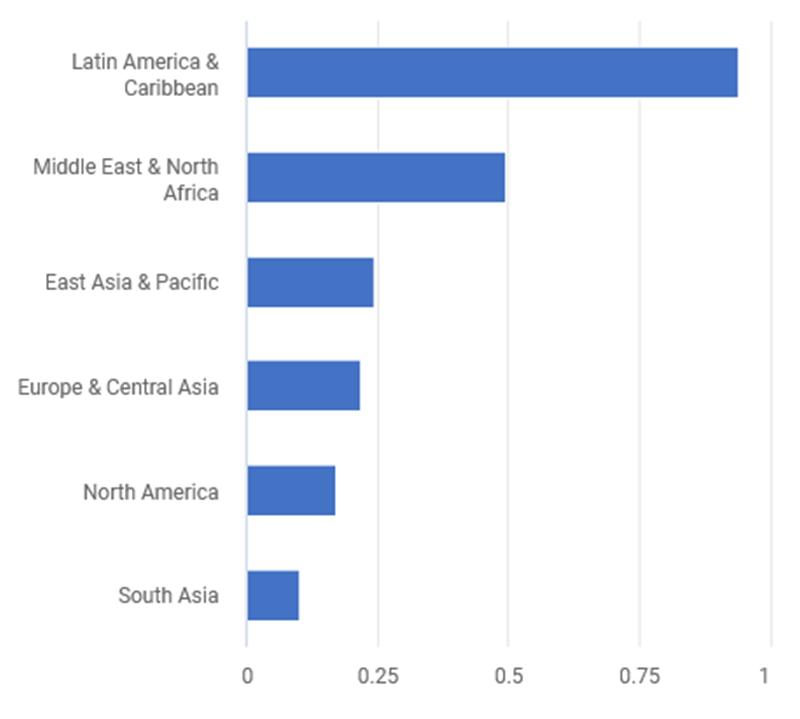

In addition, García-Bernardo and Janský study the distributional effect of MNEs’ profit shifting behavior across countries. They highlight that lower-income countries are the main losers in terms of lost tax revenue relatively to total tax revenue: MNEs shift an equivalent of 5.03% of total tax revenues from low-income countries vs. 1.01% for high-income countries. Additionally, only a few countries are found to benefit from worldwide profit shifting.

For their analysis, Garcia-Bernardo and Janský mainly rely on CbCR data published by the OECD for the 2016 fiscal year (read more). They complement it with 2017 US CbCR data, released by the Internal Revenue Service (IRS), as their coverage of US MNEs is broader than 2016 information.

In order to cope with the imperfect coverage of CbCR data they extrapolate data using a machine learning algorithm. Additional data sources include Orbis (read more), CEPII, UN Comtrade and the World Bank.

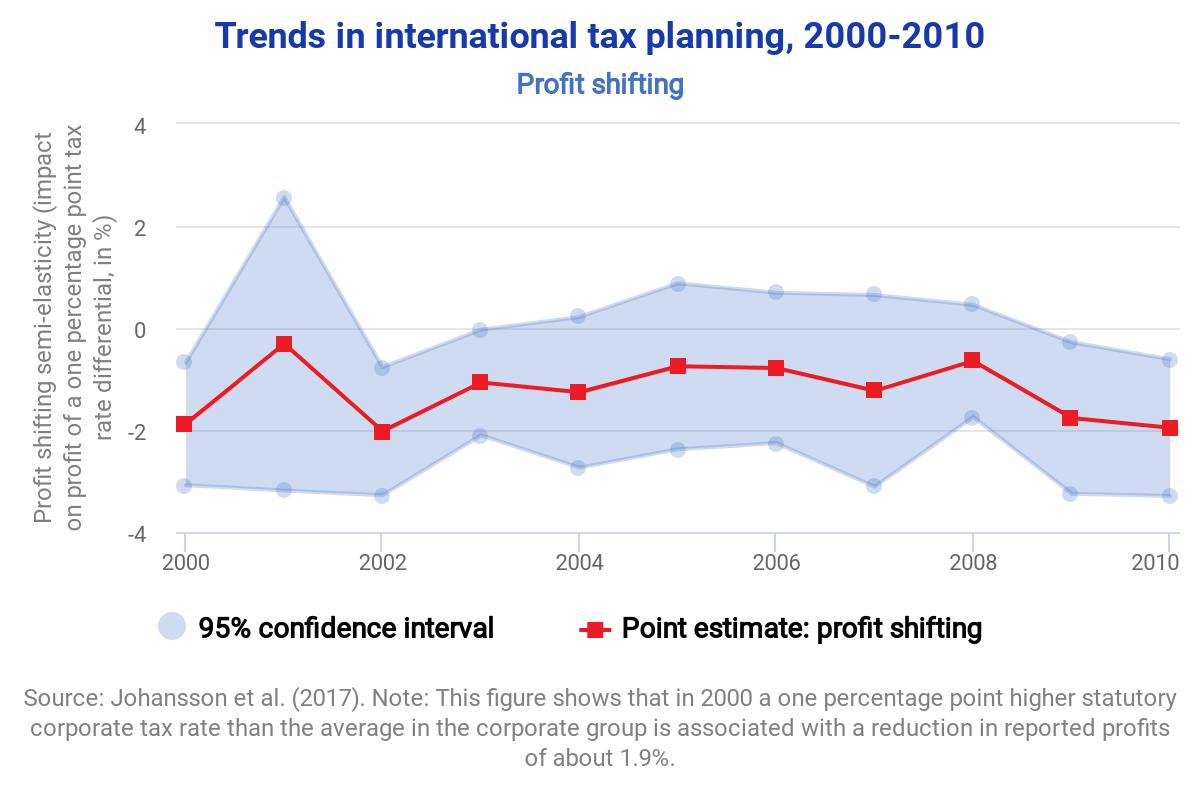

Garcia-Bernardo and Janský use a logarithmic model to estimate the semi-elasticity of reported profits with regard to backward-looking effective tax rates. They argue that the linear and quadratic models previously used in the literature tend to underestimate the semi-elasticity of profits with regard to tax rates. This is because they cannot sufficiently account for the extreme non-linearity of this relationship, i.e. the fact that MNEs shift disproportionately more profits to tax havens with zero corporate income tax than to other low-tax jurisdictions.

As an alternative, they propose a “misalignment model”. This model estimates the amount of shifted profits based on the discrepancy between the share of reported profits and the share of real economic activity (proxied by wages and employee counts, tangible assets, and unrelated party revenues) and delivers similar results as the logarithmic model.

The original working paper was published in the IES Working Paper series and it can be downloaded from the website of the IES.

The implementation of the global minimum tax in the EU

Estimating the Scale of Profit Shifting and Tax Revenue Losses Related to Foreign Direct Investment

Tax Planning by Multinational Firms: Firm-Level Evidence from a Cross-Country Database

The Missing Profits of Nations