Explorateur des rapports pays par pays publiques

Découvrez notre base de données de rapports publics pays par pays, permettant de visualiser combien les multinationales gagnent et paient…

1.1. The scale of tax avoidance

1.2. Channels of profit shifting

1.3. Countermeasures to corporate tax avoidance

2.1. The scale of tax evasion by individuals

2.2. Channels of tax evasion

2.3. Countermeasures

Explorateur des rapports pays par pays publiques

Hide-seek-hide? The effects of financial secrecy on cross-border financial assets

Tax deficits and the income shifting of U.S. multinationals

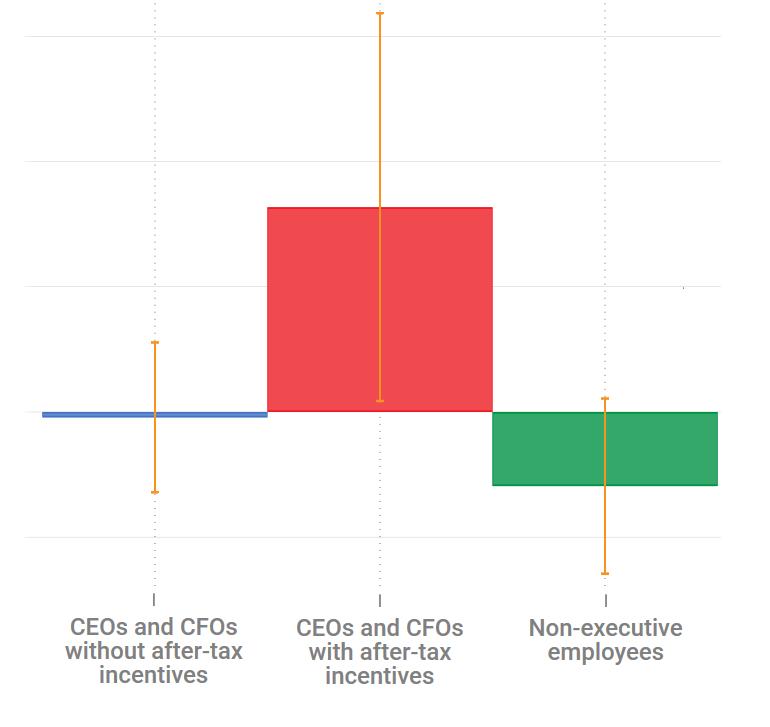

Profit shifting, employee pay, and inequalities: evidence from US-listed companies