Explorateur des rapports pays par pays publiques

Découvrez notre base de données de rapports publics pays par pays, permettant de visualiser combien les multinationales gagnent et paient…

Summary

Reiter, Langenmayr, and Holtmann investigate how German multinational banks shift profits to low-taxed affiliates by using internal debt. They use the External Position of Banks database of the Deutsche Bundesbank (2015), an administrative dataset on assets and liabilities in foreign affiliates of German multinational banks and the respective German headquarters.

As interest payments are usually tax-deductible, multinational enterprises can set up financing structures that inflate the interest payments that affiliates in high-tax countries pay to affiliates in low-tax countries, thereby reducing corporate income tax payments. While previous literature has mostly documented the strategic use of external and internal debt by non-financial firms, the authors aim at filling a gap by focusing on internal debt in the financial sector.

Using panel regressions, they find that banks use internal debt to shift profits to low tax countries, and they do so more aggressively than non-financial firms. A higher statutory corporate tax rate in a given country has a significant effect on the level of internal debt of banks in this country, which can be interpreted as evidence of tax-motivated debt-shifting.

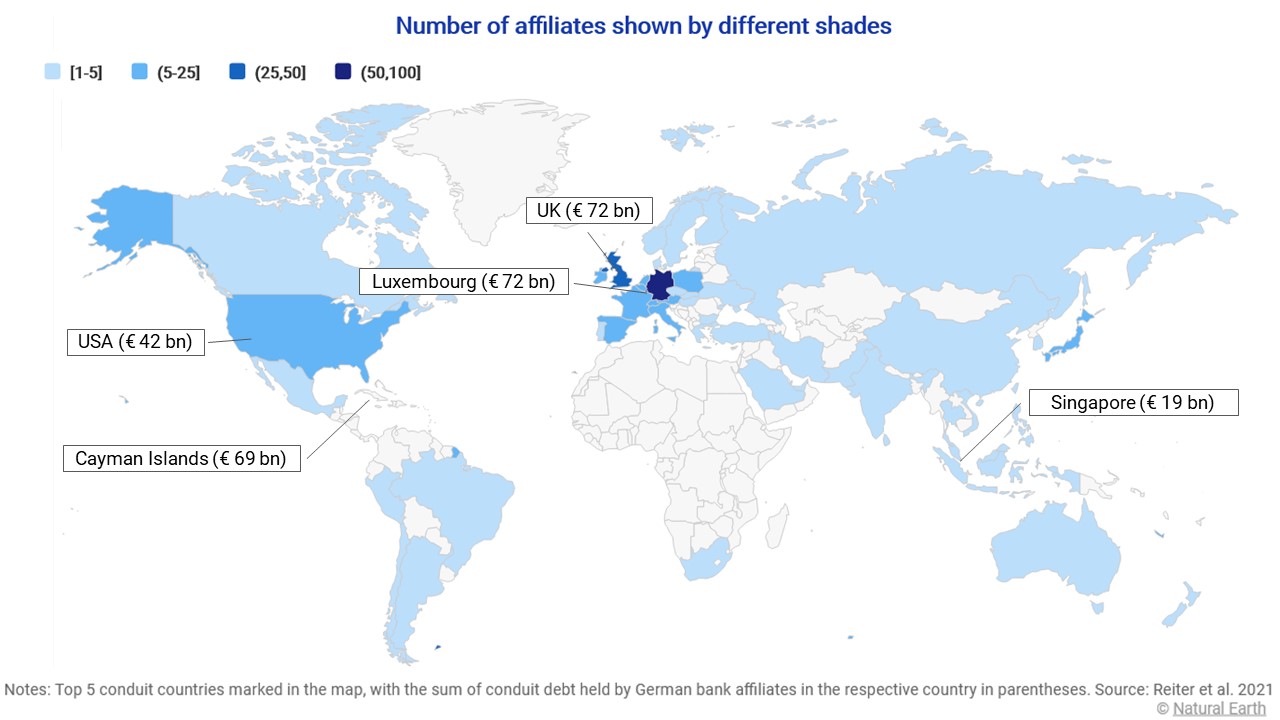

In addition, this paper sheds light on the role of conduit entities which pass through internal loans without shifting profits away from themselves. Conduit entities can serve as investment hubs in the corporate group structure but may also be used to conceal profit shifting structures or generate additional tax savings by transfer-mispricing. The authors point out that previous research on debt-shifting does not account for the double-counting of debt passed through conduit entities. As most conduit affiliates are located in low-tax countries, the previous literature has probably underestimated the extent of debt shifting. This is because the relationship between the debt level and the tax rate cannot be estimated accurately in the presence of double-counting of debt. The authors thus propose a new dependent variable, the internal net-debt-to-assets ratio, which reveals an even more intensive use of debt-shifting by German multinational banks.

Key results

Policy conclusions

Data

The authors use the External Position of Banks database of the Deutsche Bundesbank (2015), provided by the German central bank. All German banks with foreign activities are obliged to report monthly on their assets and liabilities and the assets and liabilities of their foreign branches and subsidiaries vis-à-vis non-residents. The data used are from June 2010 to December 2015. Bilateral internal loans and liabilities, separated by the country of the internal counterpart were available from July 2014 to December 2015.

Methodology

The authors estimate panel regressions using the internal-liabilities-to-total-assets ratio as a dependent variable and the statutory corporate tax rate of the affiliate as an explanatory variable. They add a set of control variables at affiliate and country level and run the regressions with and without affiliate fixed effects.

For the debt-to-asset ratio, they use gross internal liabilities of the affiliate, which is common in the literature. To better account for the role of conduit entities, the authors use internal debt net of pass-through loans as an alternative which increases the estimated coefficient of the tax rate variable.

Go to the article

The article was published in International Tax and Public Finance 28 (2021). It can be downloaded from the journal’s website. [PDF]

Explorateur des rapports pays par pays publiques

Hide-seek-hide? The effects of financial secrecy on cross-border financial assets

Tax deficits and the income shifting of U.S. multinationals

Profit shifting, employee pay, and inequalities: evidence from US-listed companies